In order to get a gauge on your business you’ll likely look at a Profit and Loss statement and a Cash Flow report. While these are similar, to get an accurate picture of how the business is performing, you need to look at Profitability as well as Liquidity.

Profit and Loss

The profit and loss report will show you Revenue earned and Expenses incurred during a period, and apply some simple math to give a Profit figure.

Note earned and incurred do not mean paid - this is often because invoices and expenses are not paid in the same period as they arise. GST isn’t usually included in your profit and loss, which sometimes makes it difficult to reconcile to actual bank transactions.

Xero Profit and Loss for Startups shows some simple math on an incurred/earned basis.

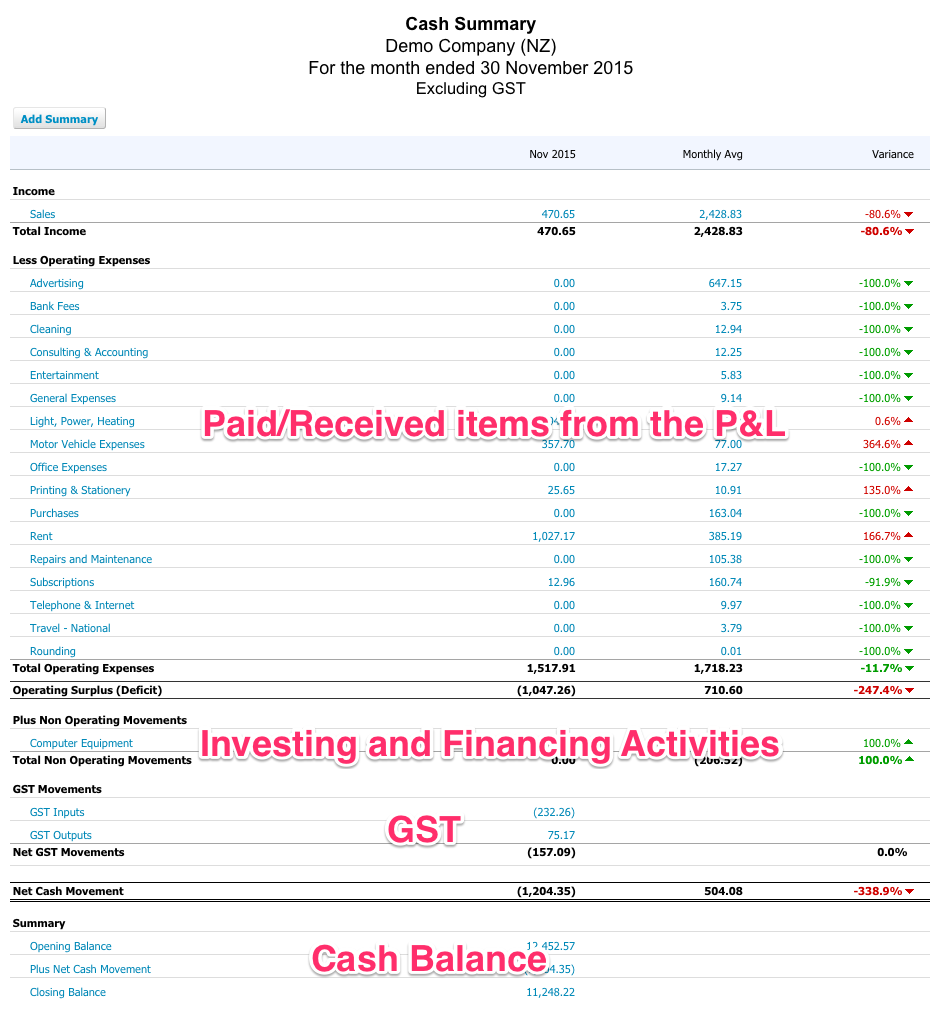

Cash Summary

This is where your Profit and Loss is translated into cash terms (when an item is paid/received) together with other movements that change your bank balance during the period.

The Cash Summary Report will show items from the Profit & Loss, other activities such as Investing and Financing Activities, GST and Cash Balances.

Other Cash Flow transactions include Investing activities (for example the purchase of assets) and Financing activities (how the business is financed through loans or equity injections). GST and Cash Balances are also accounted for separately in the Cash Summary.

While it can be useful to use only one report to get an idea of the how the business is performing, its useful to check both the Profit & Loss and the Cash Summary, as focussing on Profit only may lead to cashflow issues (customers not paying on time, suppliers not being paid) while a business run purely on cashflow misses how many expenses are being incurred and not paid, and how your revenue model works.

What does your review process look like? Not understand your numbers? Get in contact toda